By Jacques Sciammas, President, Selling to Executives

In the age of convenience, where same-day deliveries have become the gold standard and news articles are now conveniently timed down to the second, our need for accurate and concise information has never been more pressing. So why on earth do we still bother with documents numbering hundreds of pages, sans picture and color? Truth be told, 99 percent of us don’t bother reading these documents at all. They make great paperweights, but if asked about specific details, most of us might offer an uneasy grin, knowing that we have companions-in-arms, equally guilty of shirking that responsibility to read altogether.

The 10-K report: Why bother?

You’re familiar with a company’s annual report, right? But very few bother with the 10-K. And for those of you who have heard of it, do you really understand its value? Unfortunately, due to its no-color, no-graphics (thereby implying “no fun”) standard format, a format mandated by the Securities and Exchange Commission, the 10-K is easily the most overlooked, undervalued and – shockingly – untouched research document.

In my personal experience as CFO for several large corporations, where I chaired the Capital Committee (i.e., the committee responsible for overseeing purchasing decisions), I met thousands of salespeople and strategic account managers through the years, and I would say that no more than 3 percent or so had bothered going through my company’s 10-K. Now, those familiar with the 10-K may be groaning out loud and thinking, “Who is going to actually read that monstrosity?!!” And it’s true. It would be similar to “indulging” in the U.S. tax code, a document filled to the brim with dense terminology and one-dimensional creativity.

“Stop Jacques! The 10-K is tedious. I’ d never get through it, despite my and your good intentions!”

Fair enough, but let me put forth the good news [Drumroll, please!]: One doesn’t need to go through the entire document to gather the most crucial nuggets of information. While it’s true that the top executives and their legal teams are involved in the creation of the 10-K, what makes this document vital to SAMs and GAMs are the highlights (and confessions) stealthily included – and typically ignored. These highlights can assist SAMs and GAMs enterprising enough to sleuth them out to establish strong credibility and relevance with the C-level and to truly differentiate themselves from their competitors.

“OK, Jacques, you’ve caught my inter- est. So how do I leverage the 10-K to my benefit?”

Let me break it down for you: Not only does the 10-K assist you in understanding the company you’re working with, but it also provides intelligence that allows you to tap into the client executive’s mindset to uncover ideas the client is interested in and to identify untapped opportunities. It’s the executives’ insider point of view that illuminates their challenges, concerns and risk

factors in plain black and white (literally!). The 10-K also (conveniently) identifies top executives’ objectives, how these objectives are measured and how they are compensated. In other words, it can be a flashing neon path- way though utter darkness – all you need to do is follow the light home!

Interested?

“Yes!!”

Ok, then, let’s continue. According to Forrester Research, 85 percent of CXOs do not find value in their interactions with sales reps.1 In fact, many of them admit their meetings were a total waste of time. What’s ironic (tragic?) is that, in the same study, 80 percent of these same sales reps actually believe they’ve had a successful meeting!2 What the !@*? Is this just an inability by the sales rep to correctly “read the room” or something else?

I wouldn’t have believed this insane disconnect if the study had not been conducted by one of the top independent research firms in the business.

“So how do I judge if MY meeting with an executive was successful?”

Excellent question! Here are my personal guidelines. You have had a successful meeting if:

- You have presented the CXO with new (and relevant) information that provides them with value

- You have received information from the executive that illustrates not only a plan of action but continued access to the executive

- You have to do something for the CXO and the CXO has to do something for you.

This last bullet is key because, this way, he/she does not forget about you and a return seat at the table will be much easier to grab. So what do you notice about the points above? They signify an exchange, an ongoing interaction between both parties signaling their continued interest and commitment – making them priorities to one another.

“So, what is the #1 reason behind CXOs saying meetings have been unsuccessful?”

Short answer: The sales reps were not prepared. Period. Bear in mind: This doesn’t mean they didn’t “prepare.” It means they didn’t prepare for a CXO meeting. This has nothing to do with the salesperson’s intelligence or mental acuity; it merely reflects their level of preparedness as it concerns the “target”: the CXO himself. CXOs find/found that many sales reps know their industries and/or companies well, but they lacked the “X” factor.

“So how do I prepare for a CXO meeting to ensure that I bring that ”X” factor?”

You might be asking yourself, “Isn’t knowing the industry and company in question enough?” In a word: NO! You also need to know the CXO, and by this I don’t mean what cereal I usually consume with my daily paper – although I’d be impressed (and maybe slightly unnerved) if you did know this.

Understanding the CXO with whom you’re meeting means being able to answer questions revolving around their role and responsibilities within the company, uncovering their personal agenda and understanding their decision-making criteria – in addition to knowing the answers to questions facing their company and industry. A three-level research-and-preparation “pyramid” will suss out the following:

- Industry. KPIs (each industry has its own KPIs3), pressures, external fac- tors, shifting trends. This is the base of the pyramid.

- Company. Strategies, goals, challenges. This includes knowing the customer’s customers as well as your own company. Remember: The sales rep or account manager needs to be an ambassador for their own company as well. This is the middle layer of the pyramid.

- CXO. Diving into the executive in question (his or her role, responsibilities, what drives him or her). This is at the top of the pyramid.

Beware: This is not a one-size-fits-all exercise. Your prep will be different for every CXO.

Each level requires different needs to be met. For the CXO, they care about three categories of value: value to their customers, value to their firm and value to themselves.

“So, Jacques, how do You define value?”

Both the CXO and salesperson will have their own definitions of value. What is important, however, is that the salesperson understands and caters to the CXO’s meaning of value, not his own. Remember the golden rule (of sales): It’s not value unless the customer finds value in it.

“Value for the executive” comprises the following:

- Factors that positively impact the profit and loss and/or balance sheet

- Factors that improve industry KPIs as well as improve safety, security and reduce risk

- Factors that have a positive impact on employees

- Anything that provides personal value for the CXO in question

There is also value for the “indirect customer,” such as a positive impact on the customer’s customer. Lastly, there is value when dealing with broader factors overall. These include improved compliance as well as positive impact on regulatory or environmental concerns. Executives will usually compare the proposal using a “before-and-after” scenario to decide whether value exists, either directly or indirectly.

The 10-K: An overview

Yes, the 10-K is a dry, dull document required by the SEC that is basically an annual business disclosure, filed by a publicly traded company, containing “almost everything about the business that an investor would want to know.”4 This disclosure includes financial trends, changes in management, areas of concern and sources of competition, the current state of operations, and the company’s future plans.

The financial statements, specifically the income statement and balance sheet, illustrate how much money the company has made, its margins, its cur- rent debt and other important data. This enables one to “see” the state of the company’s finances.

Most of the well-known multination- als are required to file a 10-K. Foreign companies file a similar report (the 20-F), thereby providing a similar, albeit slightly less comprehensive, mea- sure of accountability.

Investopedia accurately summarized the 10-K in one sentence: “If you want to dig deeper and go beyond the slick marketing version of the annual report found on corporate websites, you’ll have to search through required filings made to the Securities and Exchange Commission.”5 The difference between the annual report and the 10-K? The first communicates what a company wants to communicate, the second communicates what the company must communicate.

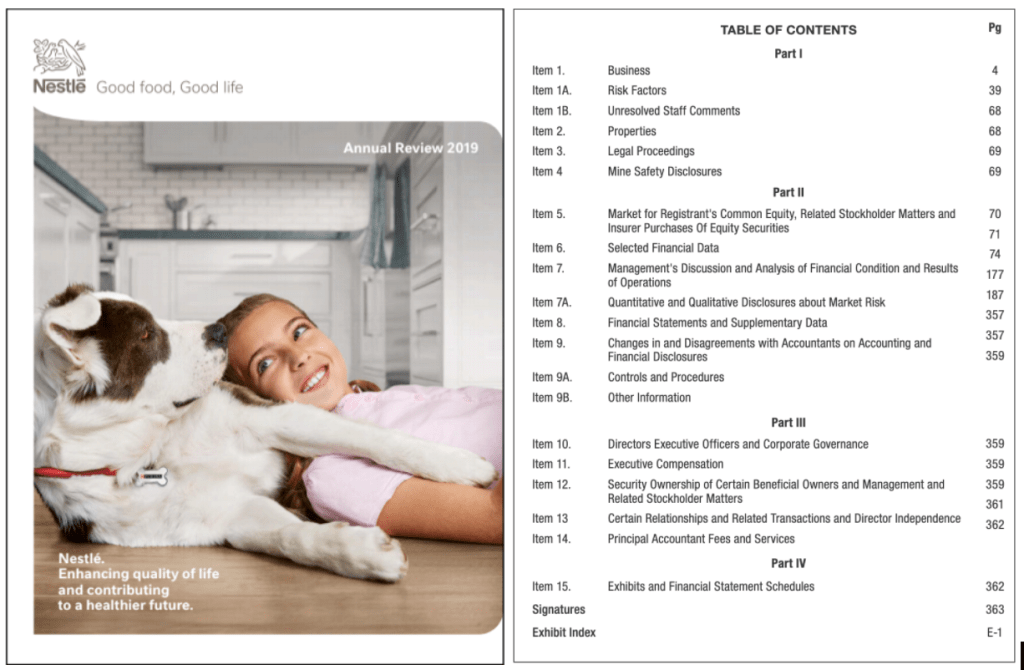

Take a look at these two images.

What do you see?

What you’re viewing on the left is the warm-and-fuzzy cover of Nestle’s Annual Report. On the right: the dreaded 10-K (courtesy of MetLife Inc.). The differences between these two documents speak for themselves. In the “boring” format comprising the standard 10-K, each Part (I, II, III, IV) must be filled in. If you’re not in the mining sector, for example, Part I, Section 4, may not apply to you. But you’re still required to fill it out as “not applicable.” Again, every section is required by law for all U.S.-based publicly traded companies.

This document can run anywhere from a hundred to four hundred pages, and it requires input and sign-off of the CEO, the CFO, and both the legal and management team.

The most important sections of a 10-K report

Consider these the “VIP” sections:

- Part I – Risk Factors

- Part II – Management Discussion and Analysis

- Part III – Executive Compensation (also called “Remuneration” or “Compensation”)

Take a look at the 10-K filing for MetLife Inc. Items 1A, 7 and 11 are the most important sections to note, and, interestingly enough, these are the same sections most GAMs and SAMs religiously ignore. They typically pay attention to items 1, 6 and 10 – basically everything that’s included in the annual report anyway.

Risk Factors

This is located under the “Business” section and covers regulatory, political, macroeconomic, industry, strategic and operational risks. My tip: focus on strategic and operational risk factors.

Case: Ford Motor Company

Item: Operational and strategic risk factors.

Look on page. 12 of the 10-K report linked above. Here, the company provides intimate details concerning areas that require improvement!

I have highlighted crucial details concerning Ford Motor Company’s operational and strategic risk factors.

“Operational Systems, security systems and vehicles could be affected by cyber incidents.”

“Despite security measures, we are at risk for interruptions, outages and compromises of …operational systems and manufacturing processes.”

If a security company picked up on these vital details, they could approach Ford Motor with a viable solution. One should also pay attention to the “priority” of the risk factors listed for previous years versus the current year. If a risk factor was previously listed as #5 and has now moved up to #1, this is obviously causing executives a great deal of concern.

Management Discussion and Analysis (MD&A)

This section focuses on key challenges faced by the company, demands made on the business, commitments to other parties and uncertainties the company faces, including their implications and significance to the business itself.

Case: Metro AG

As an example, I’ve distilled Metro AG’s MD&A to the following key points, where the company discusses simplifying its activities, structures and processes.

“We are also planning to implement a number of efficiency measures, in particular the simplification of administrative structures, processes and business activities.”

“This includes… development of new channels and customers as well as an increase in customer loyalty, and an associated enhanced exploitation of customer potential, for example, through digital solutions.”

If we really think about what is written, it basically tells us that an overwhelming number of businesses are bogged down by overly complicated or inefficient procedures that waste valuable time and resources. This is a cry for help, calling out to solution providers for assistance. Translation: This is a ripe opportunity.

Executive Compensation

Possibly the most important of all three sections I’ve listed, “executive compensation” refers to the manner in which the CEO, the CFO and usually the company’s three highest-paid officers are compensated – i.e., how they earn their fat bonuses. To be clear, we’re not looking at how much they’ve earned but rather how they’ve earned it by analyzing their short- and long-term incentives, specifically the KPIs that drive their compensation.

Take a look at Ford Motor Company’s Proxy Statement for 2020 below.

The chart illustrates that Ford’s top executives are compensated based on revenue growth, free cash flow, EBIT (earnings before interest and taxes) margin and quality. Analyzing the above, we see that the company exceeded its quality goal (118% of target) but totally missed out on its revenue goal (4% of target!). When applying this critical piece of information to a real-life scenario, the sales rep should target the weaker areas that require improvement—i.e. solutions that would help sell more cars and trucks to increase revenue–rather than focusing on an already successful target (i.e., quality). The CXO is interested in both, but one (revenue growth) has a much higher priority as it’s a major pain point.

“OK, Jacques. But how do I introduce these concerns in conversation with the CXO?”

Present yourself as the solution! You’ve already rooted out the most pressing concerns faced by the company executives, now it’s time to bring it home. Align your value proposition with concerns divulged in the 10-K, and don’t mention “the money.” Instead, focus on the impact your solution(s) can provide.

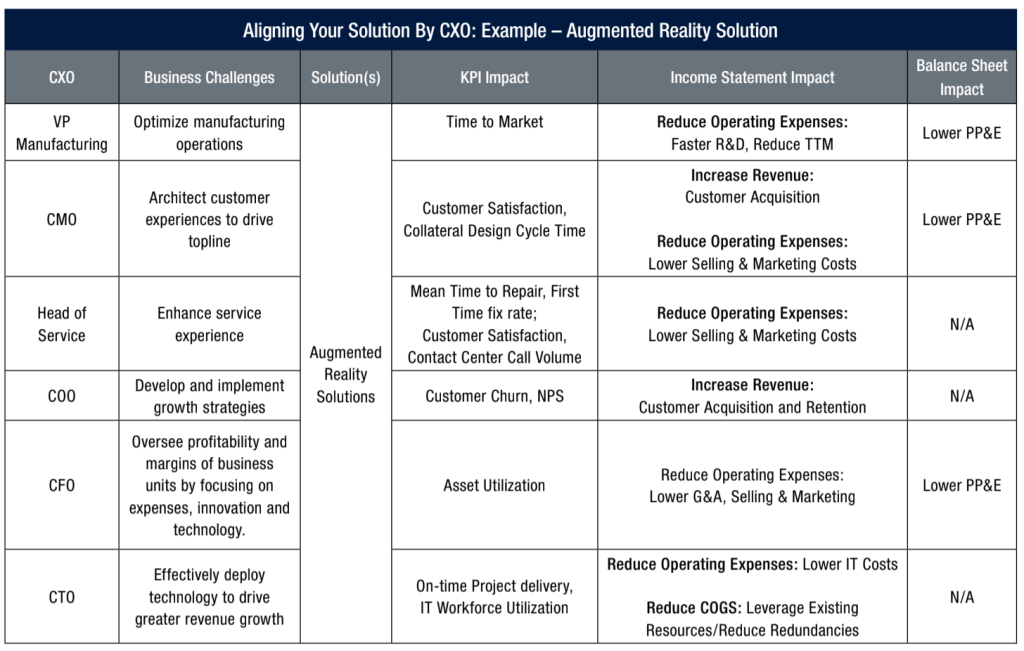

Tailor your solution to concerns relevant to the company AND to the executive you’re dealing with. Remember, each executive is concerned with a different role and challenge.

Compare the chief marketing officer with the vice president for manufacturing in the table “Aligning Your Solution By CXO.”

The former is challenged with increasing customer revenue, acquisition and retention, while the latter is primarily occupied with reducing operating expenses and optimizing the manufacturing operations. Incorporate creativity and out-of- the-box-thinking strategies to win over the executive you’re targeting. You may be using the same solution for multiple executives, but utilize a different message, one that’s relevant to each CXO.

“Any other areas or tips you have on research and preparation?”

So glad you asked! I do.

Research and prep: Additional information

- Private companies and disclosure: Unlisted companies do not require a 10-K or 20-F, so when trying to close a private company, look at its closest competitors in order to root out information. Everyone competes on the same landscape (more or less!), and, by studying the closest public competitors, you can gauge where said private company’s concerns and priorities lie.

- Quarterly call with analysts: a MUST-have requirement, the best one-hour investment of your time.

- Consult the research analyst reports

- Review your own company’s 10-K/20-F

“So, what do you recommend Jacques?”

- Review key sections of your accounts’ 10-K/20-F

- Review latest quarterly analyst call

- Identify new opportunities based on risk factors and MD&A

- Map your proposals tailored to the relevant CXO’s operational and finan- cial KPIs noted in the executive compensation section of the 10-K/20-F

Once you master the above, you will not only differentiate yourself from over 95 percent of the existing salesforce, you will gain credibility and trust from your client executives and, ultimately, close more impressive deals faster than imagined. Good luck!

Jacques Sciammas has held the roles of Chief Operating Officer and Chief Financial Officer for several global corporations, where he directed executive buying decisions and vendor selection for over 25 years. He has conducted over 400 workshops and keynotes around the globe to help sales teams gain better access, interaction and maintain excellent long-term relationships with their Clients‘ Senior Executives.

Any questions or comments, please feel free to contact Jacques at jacques@sellingtoexecutives. com or Tel: 011 33 6 23 01 14 38 www. sellingtoexecutives.com. All rights reserved.